Curve And The Convex Wars

Did you know that we have an Ambassador Program?

Today we are pleased to present you a piece of content that was prepared by one of our ambassadors about Curve and the Convex wars

DeFi protocols used to compete for the control of veCRV, the governance token of Curve. As Convex gained the upper hand, a new stage of this DeFi ‘war’ began — this time for the control over Convex itself

WHAT IS CURVE

CURVE is a decentralized exchange like Uniswap or Sushiswap, but with an important caveat special swapping them an exceptionally efficient platform compared to other DEXes.

Before 14 the May’22 crypto crash, Curve had a TVL of $20 billion across 9 chains, making it the largest AMM (automated market maker) in all of DeFi. . In April 2022 alone, Curve’s TVL increased by 19%.

Curve was set up in early 2020. From the beginning, it was a highly efficient decentralized Ethereum DEX designed for stablecoin trading. Curve managed to dramatically reduce price slippage when swapping stablecoins, thus enabling much more efficient trades than on Uniswap. The problem with Uniswap was that its “Constant Product Formula” (x*y=K) only worked great for trades that used a small amount of the total liquidity in a given pool. By contrast, a large trade could have a significant price impact.

For Stable coins, this was a particularly serious problem, because it made it very expensive to swap between tokens like USDC and DAI, which should be worth the same.

Curve modified the Constant Product formula to minimize slippage and soon became the go-to platform for swapping between stablecoins. Its daily transaction volume routinely exceeded $1 billion, sometimes coming close to $2 billion. In fact, it even spiked a little during bearish periods in the market, since many people needed money quickly, covering their leveraged position.

CURVE’S TOKENOMICS

High trading volume This brings in a lot of traffic, especially from Whales, which High trading volume also means a lot of fee rewards for liquidity providers. For every trade that occurs on Curve, liquidity providers earn a percentage of the fee in the form of $CRV.

They can then lock the CRV to get veCRV (vote-escrowed CRV). The lockout period varies between 1 week and 4 years. The system is designed to provide 1veCRV per 1CRV for a 4-year lock-in, 0.5 veCRV for a 2-year lock-in, and 0.25 veCRV when locking up for 1 year. Thus, the longer you lock, the higher bonus rewards you will get while providing liquidity on a pool.

Once you lock your veCRV, you will not be able to retrieve it until the lock period expires, but Curve will pay you additional CRV in proportion to the duration of the lock-in period.

On top of these rewards, veCRV holders can vote to select the pools that will receive CRV boosts — yet another source of rewards for the liquidity providers in those pools. Thus, unlike most reward tokens, which are extremely inflationary and have no use cases aside from governance, $CRV offers a lot of additional utility.

The rights obtained by locking your CRV for veCRV

🌀 Governance

veCRV holders have the power to influence which pools get additional CRV boosts. They can also vote on any proposal made by the Curve DAO. It can be a change in the list of y pools, a proposal for a new pool, or additional CRV rewards for locking cash into a pool. The more veCRV a user locks in, the more power they will have over the vote.

The fun part is that the more CRV you hold, the more veCRV you can get, and thus the more control you’ll have over the emissions on Curve and boost distribution.

Recently, Curve had a lock-up rate of almost 50% of all the CRV in circulation, with an average lock-up period of 3.63 years. The full emission of Curve tokens will be complete in 30 years, but the Curve emission strategy is still very aggressive, as it’s inflating at a very high rate. The reason it’s not resulting in a complete dump of the token’s value is that holders keep locking it up for 4 years.

Convex and the Curve Wars

As veCRV holders decide who gets the boosts, they represent an asset for any DeFi protocol that wishes to increase the rewards in its pool and therefore its TVL. This is the origin of so-called bribes: protocols paying CRV holders additional rewards to attract their liquidity and votes. The most successful of these protocols is Convex.

One could describe Convex as a layer between governance and returns on veCRV. In April 2021, Convex launched a sort of a bribery game, offering veCRV holders a 1% airdrops of its CVX tokens in exchange for their support.

Soon Yearn Finance joined the competition against Curve to secure as much veCRV as possible — and therefore the most voting power over Curve Finance. This competition came to be known as the Curve Wars, as it was Convex Finance that eventually managed to secure approximately 47% of the total amount of veCRV in circulation.

THE DOMINANCE OF CURVE’S TVL BY CONVEX and the Convex Wars

Convex’ victory had a great impact on Curve’s valuable governance vote. 85% of the Curve TVL is now routed and pledged through Convex.

*Recently, the Curve Wars for the governance of Curve have been gradually evolving into a “Convex War” over the governance of Convex — essentially. Instead of luring in CRV holders to obtain control over their veCRV and voting rights, protocols directly bribe the holders of Convex’ vlCVX tokens, which are locked for 16 weeks, which gives them control over the underlying veCRV governance power of Convex.

This way, each vlCVX holder received around $2.75 for each locked CVX since September 2021.

*Source: https://members.delphidigital.io/reports/convex-wars-opensea-recovery-nft-endorsements/

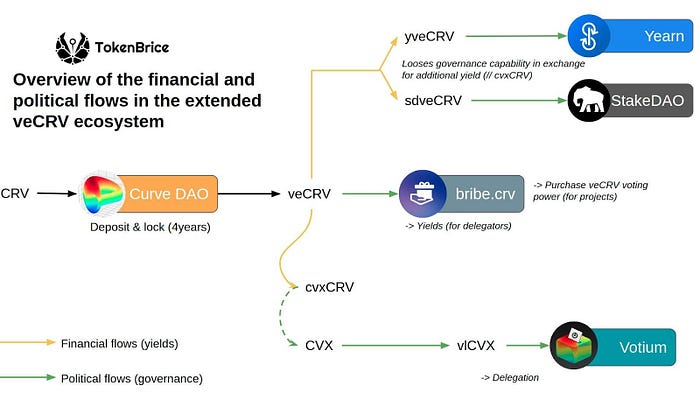

An overview of the ecosystem built on veCRV

*After a somewhat timid start, tokenized incentives are being used more and more, and many projects are now proposing bribes. The returns in the first few weeks have been excellent, though it remains to be seen if they will last. For example, some holders earned a 10% return on their veCRV in 5 weeks by voting for the MIM pool and receiving SPELL tokens in bribes.

*Source: https://www.btcfans.com/en-us/article/72141

💨 So far the bribe game has focused mainly on CRV, but other tokenized incentive services are also in development.or example, Paladin intends to offer a similar mechanism for other protocols as well asIn addition, Convex Finance will also feature Frax Finance’s veFXs and veCRV, granting agreement governance rights and voting rights on the Frax instrument.

Pontem is paying close attention to this space. We are partnering with Aptos, the safest and most scalable Layer 1 blockchain which is based on the Move Language and built by a team of former Diem engineers. Pontem will be leading the development of foundational DeFi tools such as AMMs, stablecoins, and an Implementation of the Ethereum Virtual Machine, as well as a development toolset. Pontem is deeply interested in a custodial future, in which broader market access can be achieved by simplifying DeFi tools and automating processes

To stay updated on our work, be sure to follow Pontem on Twitter, subscribe on Medium, and connect with us on Telegram